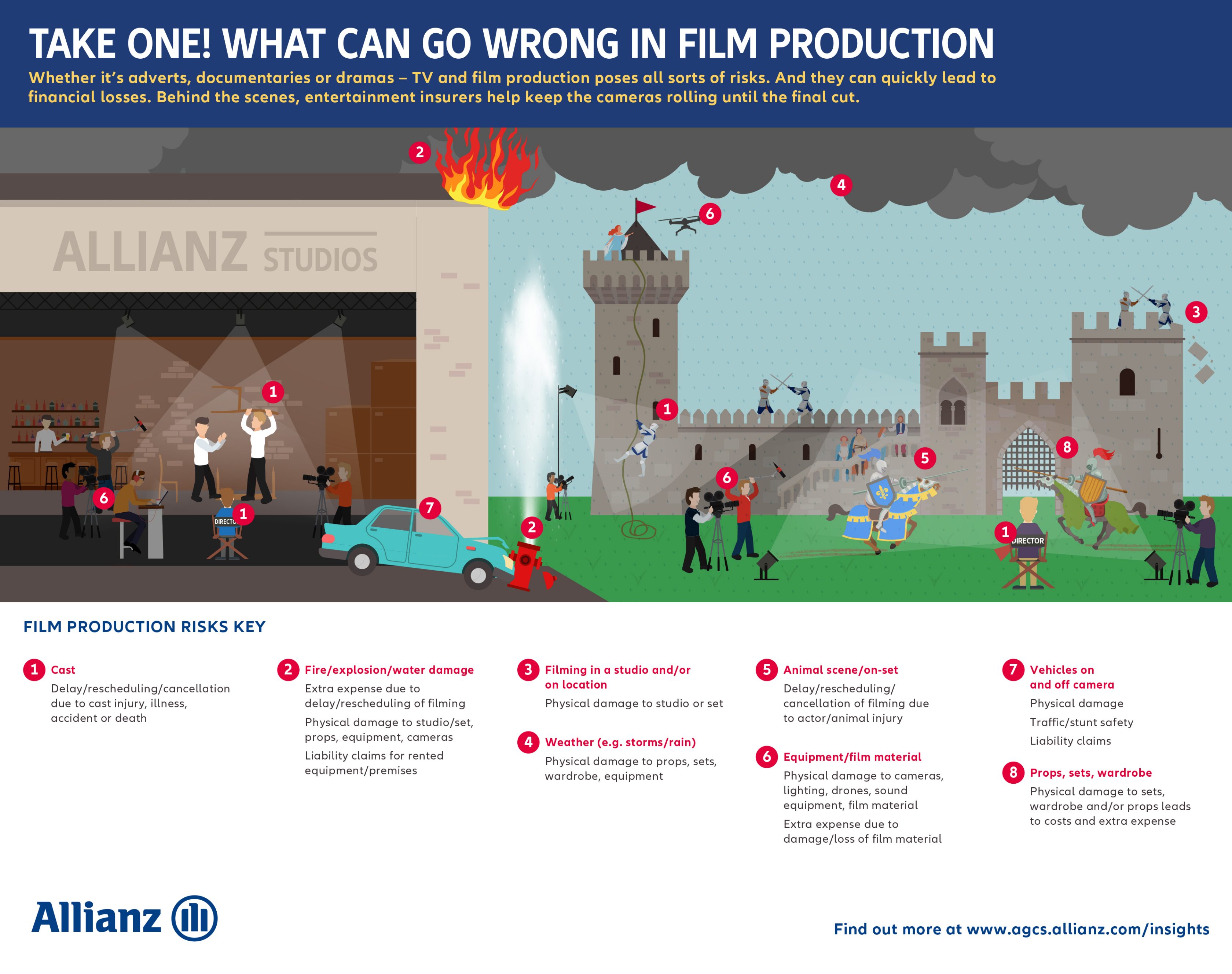

Digital technology, visual effects, extravagant live events and other trends are changing the industry.

- By far the most prevalent cause of interruption is an illness or accident to a cast member

- Injury to a major star can delay the production, leading to multi-million dollar claims

- Proliferation of visual effects means interruptions can bring expensive claims

- Live events is fastest growing area of industry but increasing complexity brings new interruption risks

Two different contingency coverages make-up typical BI protection in the entertainment sector. The first is cast member coverage under the film/television production package, or performer nonappearance under the live event contingency package. This cover provides indemnity for additional costs incurred due to production interruption, postponement or cancellation due to accident, illness or death of a declared cast member/ performer.

“Some productions can have a $200m budget with daily operating costs running between $400,000 to $500,000,” explains Ian Galloway, Senior Director Entertainment Claims & Risk Services AGCS. “So any interruption is costly.”

The second time element coverage involves extra expense for other circumstances that could interrupt scheduled production, usually related to property damage to facilities or equipment or actions of a civil authority that prevent access to property or facilities.

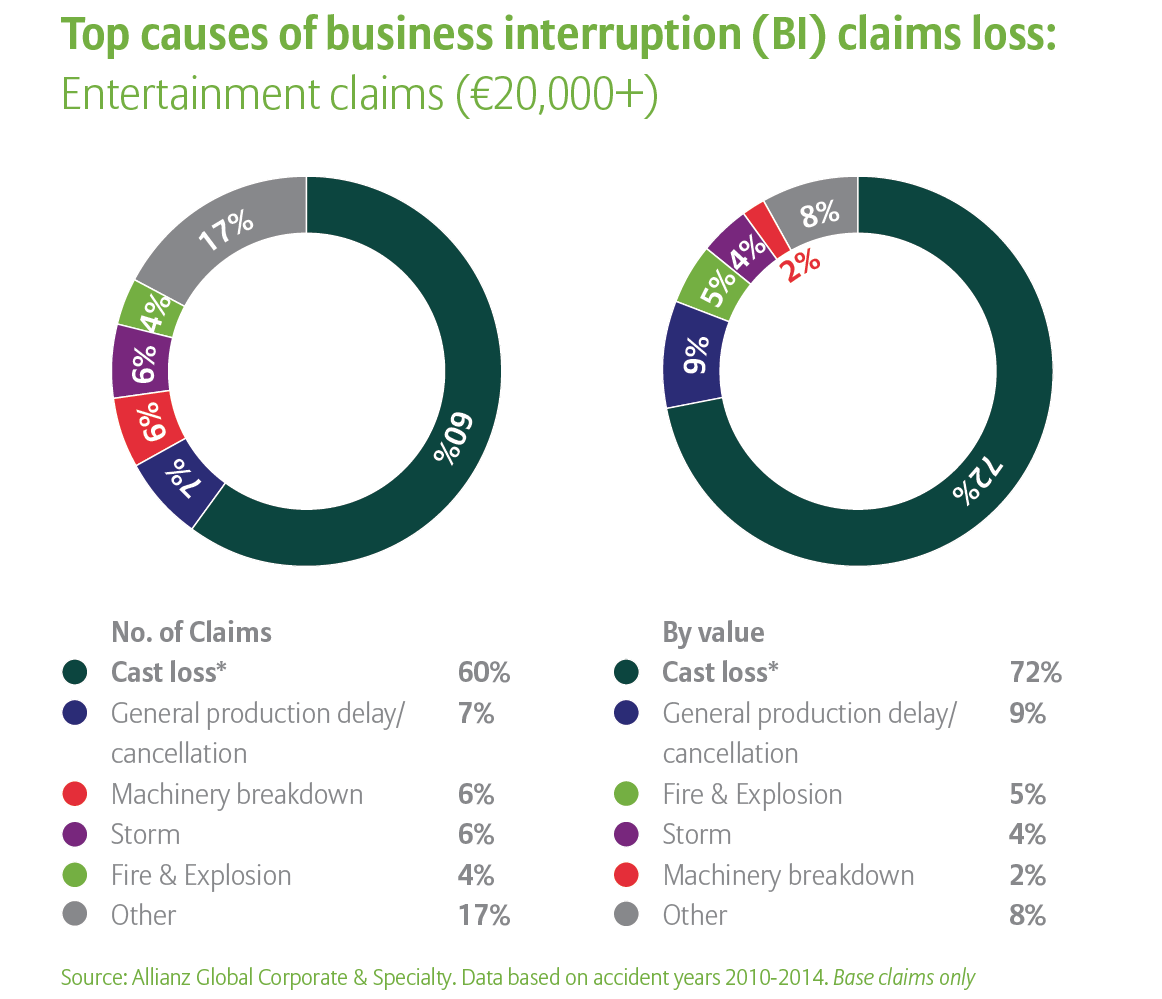

BI losses due to cast member illness or accident

By far the most prevalent cause of interruption claims in the entertainment industry is an illness or accident to a cast member.

“Extensive medical background checks of all declared talent is standard in the underwriting phase,” explains Galloway. “However, potentially more risky stunt activity and scenes involving pyrotechnics or car chases require extra scrutiny by risk engineers trained in live effects.”

To illustrate the importance of coverage against performer illness or accident, consider the example of a major star filming overseas who broke a bone that required extensive surgery and recovery. Since the person was the principal cast member featured in almost every scene, the show literally could not go on. Significant costs accrued as a result of delay and a large claim in the many millions was settled with the studio.

Another example occurred in the death of two cast members working on different films. In one case, no interruption was suffered because the performer had completed filming and post-production work and only slight changes to the script were required. The death of the other performer, however, delayed the schedule since they were the principal talent, requiring significant re-shoots.

“Claims paid in that case were substantial,” says Galloway.

*What is cast loss? Cast loss refers to when a cast member or performer is unable to perform.

Visual effects

The biggest change with film and television has been the proliferation of visual effects and technical requirements that change from shoot to shoot. Galloway explains: “Underwriting complex, computerized visual effects is challenging, to say the least.”

“In the past, visual effects were added during postproduction and didn’t impact shooting. These days, effects are integral to principal photography. Risks are high due to financial impacts of visual effects.”

Typically, studios contract with third party companies that employ scores of technicians to take daily scenes and apply effects. A film’s shooting timeline takes into account this activity and factors production delay into the contractual obligations a studio has to third party vendors. An idle visual effect shop is a significant and expensive delay.

“The principal cast member of one recent action movie, for example, broke a bone and delayed shooting for a considerable amount of time,” says Galloway. “The backend obligations the studio owed to the visual effects shop were considerably more than shut-down costs.”

Technology – the new Hollywood star

From a claims handling perspective, the most challenging issue facing the industry today is keeping up with fast changing technology. Upgrading old equipment is the most challenging and expensive aspect of the business. In the last 10 to 15 years, the industry has transitioned from analog to digital. Most old equipment needs replacing. Digital medium is easier to work with, less labor intensive and insusceptible to decay or x-ray destruction.

“Ten years ago one of the most prevalent types of claims was film negative accidentally destroyed by airport x-ray machines,” Galloway says. “Such claims are practically unheard of today.”

Also, footage shot digitally can be viewed on set almost immediately to check for quality, allowing for immediate reshoots while all cast, equipment and sets are in place, reducing increased costs for later reshoots.

“There’s no question digital is better,” says Galloway. “But equipment upgrades from analog to digital represent extensive studio expense.”

The most impactful trend as a result of frequent upgrades is that in the event of property damage insurance coverages repay the cost of lost or damaged older equipment. Claimants expect upgrades to digital equipment, which is obviously much more expensive.

Weather is important claims driver

From a claims handling perspective, the most challenging issue facing the industry today is keeping up with fast changing technology. Upgrading old equipment is the most challenging and expensive aspect of the business. In the last 10 to 15 years, the industry has transitioned from analog to digital. Most old equipment needs replacing. Digital medium is easier to work with, less labor intensive and insusceptible to decay or x-ray destruction.

“Ten years ago one of the most prevalent types of claims was film negative accidentally destroyed by airport x-ray machines,” Galloway says. “Such claims are practically unheard of today.”

Also, footage shot digitally can be viewed on set almost immediately to check for quality, allowing for immediate reshoots while all cast, equipment and sets are in place, reducing increased costs for later reshoots.

“There’s no question digital is better,” says Galloway. “But equipment upgrades from analog to digital represent extensive studio expense.”

The most impactful trend as a result of frequent upgrades is that in the event of property damage insurance coverages repay the cost of lost or damaged older equipment. Claimants expect upgrades to digital equipment, which is obviously much more expensive.

Live event risks

Live events are among the fastest growing areas of the industry. Ranging from outdoor amphitheater or small venue shows to sold-out stadium concerts, including music festivals like Lollapalooza, which takes place in six countries across three continents, live event risk management is a specialist topic of consideration.

Claims settlement for live events is less traditional than cast member/performer nonappearance. During concerts crowds can become aggressive, especially as they “mosh” to get as close to the stage as possible or pack together tight enough to allow “crowd surfing” to occur.

The occupant load on the main floor can overwhelm the most aware security team. At the same time venue owners, managers and security personnel face a number

of risk exposures on- and backstage. Electric wires, ropes, pulleys, temporary sets, and a multitude of other elements can make the area frequented by performers among the most risky areas of a venue.

With live events, the single highest insurance concern is the quality of the singing voice. Performers in a live setting can still sing with a broken leg, but not with laryngitis. The former might not trigger a claim; the latter likely would.

Claims best practice: The importance of claims reporting

When an accident or incident occurs, reporting the claim as soon as possible is key, according to Ian Galloway, Entertainment Claims Specialist at AGCS.

“We have a wealth of experience on our claims handling team,” he explains. “But we need to work immediately with our insured to begin mitigation.”

He continues: “An example of this would be an injury to a cast member. If given enough warning, we can look at the schedule and see if rearranging scenes will work, for example, shooting the ones in which the cast member doesn’t appear. That can be the most cost effective solution to shutting down production altogether.”

Little magic would appear on the silver screen if it was not for the security that insurance provides to filmmakers.

Newsletter

Keep up to date on all news and insights from AGCS

Allianz Group companies

Allianz operates as an international insurer on almost every continent. Find Allianz in your own country/region.

AGCS offices

With the Allianz network AGCS provides services in over 200 countries and territories.