Report | July 2022

Global Claims Review 2022

The Global Claims Review from Allianz Global Corporate & Specialty (AGCS) is a report examining developments in corporate insurance claims and highlighting the top causes of loss for companies and other emerging trends to watch.

Summary

Businesses must navigate an increasingly complex risk landscape. As well as having to combat the threat posed by natural catastrophes and man-made hazards, companies must deal with the demands of a less forgiving regulatory and legal environment, emerging risks posed by our growing reliance on technology and, of course, the challenges that issues such as the Ukraine conflict and rising inflation bring. All of these factors can combine to impair successful running of operations. Insurers have a vital role to play in ensuring any disruption following a loss event is minimized.

Global claims trends

The report highlights the increasingly high values at risk in corporate insurance claims. AGCS has identified the top causes of loss and emerging trends from more than 530,000 insurance industry claims in over 200 countries and territories with which it has been involved between 2017 and 2021. These claims have an approximate value of €88.7bn, which means that insurance companies have paid out – on average – over €48mn every day for five years to cover losses – outlining the important role the sector has to play in helping businesses manage and mitigate such perils.

Claims payments can vary enormously in scale reflecting the widespread nature of the risk landscape. Significant corporate insurance claims (>€100mn) such as those arising from fires, aviation crashes or shipping incidents for example, account for fewer than one per cent of claims by number, but for more than a quarter (€24.6bn) of the total value of all claims analyzed. Conversely, around 88% of claims are valued at or below €50,000, accounting for just three per cent of total value.

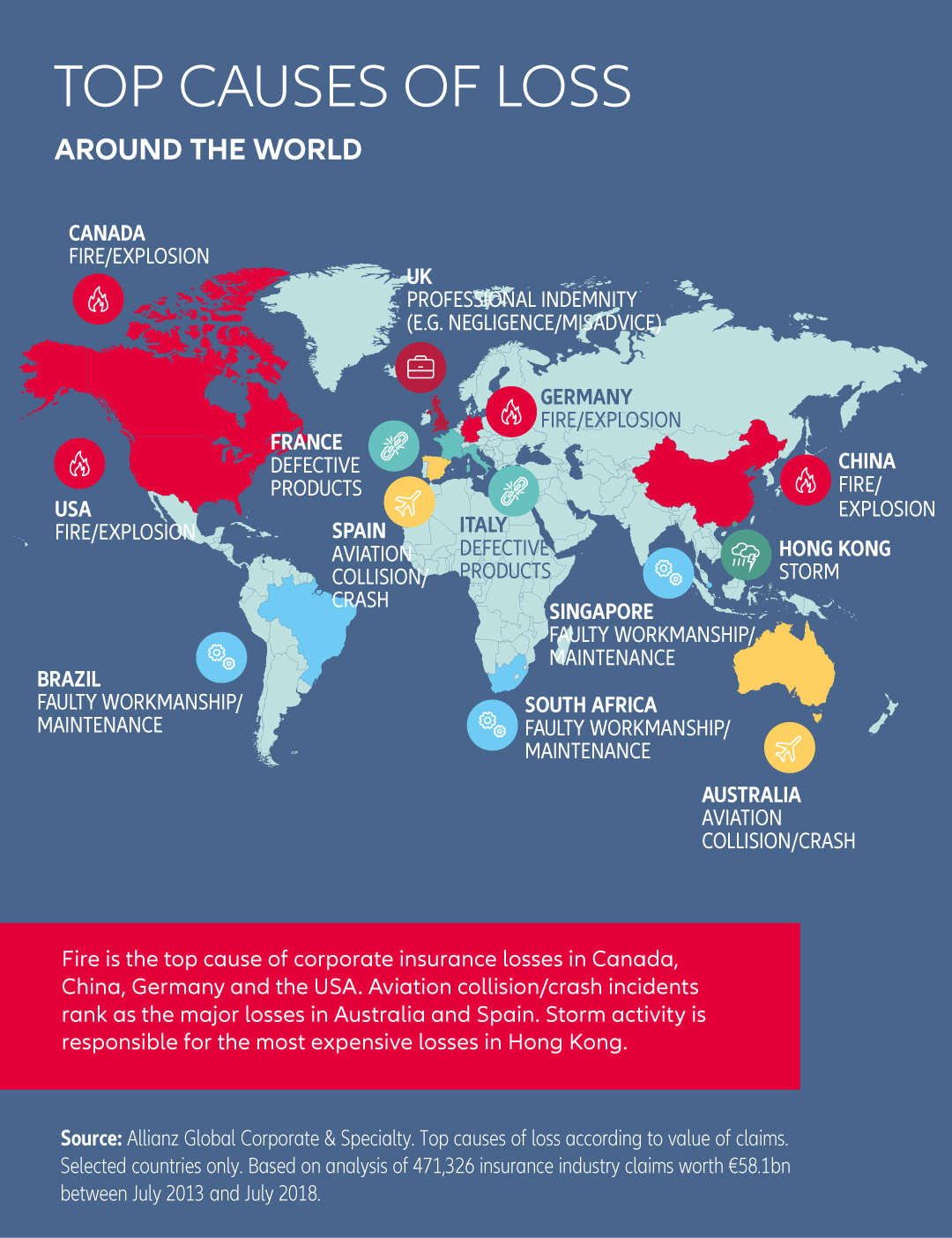

The top 10 causes of loss

The analysis shows that almost 75% of financial losses arise from the top 10 causes of loss, while the top three causes account for close to half (45%) of the value. Despite improvements in risk management and fire prevention over the years, fire/explosion (excluding wildfires) is the largest single identified cause of corporate insurance losses, accounting for 21% of the value of all claims.

During the past five years such incidents have caused in excess of €18bn worth of insurance losses from over 12,000 claims and are responsible for 13 of the 20 largest non-natural catastrophe loss events analyzed. Even the average claim from such an incident totals almost €1.5mn. Claims are becoming more severe due to factors such as higher property and asset values, more complex supply chains and the growth in concentrations of exposures. Costs associated with the impact of business interruption following the aftermath of a fire can significantly add to the final loss total of an incident, given the time it can take to get production back up and running at a large manufacturing plant, while soaring inflation will only challenge claims costs further.

Natural catastrophes (15%) ranks as the second top cause of losses globally by value of claims. Losses continue to rise with climate change and changes to exposures (such as increasing economic activity in natural catastrophe zones).

Analysis of more than 20,000 claims around the world, with an approximate value of €13.7bn, shows that hurricanes/ tornados are the most expensive cause of natural catastrophe loss, accounting for 29% of the value of all claims, driven by the fact that two Atlantic hurricane seasons out of the previous five (2017 and 2021) now rank among the top three most active and costliest seasons on record. Collectively, the top five causes of loss – hurricanes/tornados (29%); storm (19%); flood (14%); frost/ice/snow (9%) and earthquake/ tsunami (6%) account for 77% of the value of all nat cat claims.

Insurers are also seeing new and more unusual loss scenarios. During 2021, the ‘Texas Big Freeze’ in the US and flooding in Germany stand out as events that were both large but had unexpected claims. For example, the ‘Texas Big Freeze’ in February caused huge disruption to infrastructure and manufacturing, with many companies forced into temporary shutdowns by widespread power outages, bringing some large contingent business interruption losses. The event is estimated to have caused economic losses up to $150bn, while Winter Storm Uri caused $15bn in insured losses nationwide.

Top 10 global causes of loss by value of claims

Based on analysis of 534,456 business insurance claims between January 1, 2017, and December 31, 2021, worth approximately €88.7bn in value. “Other” causes of loss account for 26% of the value of all claims. Claims total includes the share of other insurers in addition to AGCS.

Source: Allianz Global Corporate & Specialty

Faulty workmanship/maintenance incidents are the third top cause of loss overall (accounting for 9% by value) and are also the second most frequent driver of claims (accounting for 7% by number). Costly incidents can include the collapse of building/structure/subsidence from faulty work, faulty manufacturing of products/components; or incorrect design.

Aviation collision/crash incidents (9%) are the fourth top cause of losses globally. There are many losses which fall within this category in addition to a major airplane crash however. These include damage to aircraft caused during ground handling incidents; over- and under-shooting runways; making an emergency or forced landing or even damage caused by a bird strike.

Top causes of loss by total value of natural catastrophe claims

Based on analysis of 22,850 natural catastrophe claims between January 1, 2017, and December 31, 2021, worth approximately €13.7bn. “Other” causes of loss account for 23% of the value of all claims. Claims total includes the share of other insurers in addition to AGCS.

How inflation is impacting claims

“Replacement costs more, replacement takes longer”

Thomas Sepp, Chief Claims Officer and Member of the Board of Management at AGCS

AGCS Chief Claims Officer Thomas Sepp answers the pressing questions on how inflation is impacting claims and why the undervaluation of assets is a key concern for both insurers and policyholders.

"Inflation was running hot even before Russia’s invasion of Ukraine, driven by higher commodity prices, supply-chain interruptions, and high energy prices. The war in Ukraine caused further price shocks for a wide range of commodities, energy, and food. As a corporate insurer, we find several specific inflationary trends particularly alarming, and we are closely monitoring how price indices for energy, raw materials, and construction costs are developing because these have an immediate impact on businesses and on potential claims.

It is now much more expensive to repair or rebuild damaged property. The cost of construction is soaring in many countries due to higher prices for energy and raw materials. [...] In addition, materials are not only significantly more expensive but often simply unavailable due to logistics, shipping and supply-chain bottlenecks."

Download the report

Simply fill out the form below to receive an email from us with the link to the full report.

Enjoy reading!

Fields marked with asterisk (*) are mandatory.

Previous report

The coronavirus outbreak has posed a unique test for commercial insurance claims. Historical patterns have been upended, while claims teams have had to maintain service levels during a period of significant operational challenges.

This report from 2020 identifies some of the new claims trends that have materialized as a result of the virus, assesses the prospect for future notification activity and highlights how claims teams have responded in this new environment.

Claims issues to watch

Further claims issues to watch & related news

Newsletter

Keep up to date on all news and insights from AGCS

Further information

Your regional claims contacts

Global Claims trends to watch in 2022

Thank you for joining our webinar on August 17, 2022

What are the 10 biggest causes of loss suffered by companies around the world over the past five years?

AGCS Chief Claims Officer Thomas Sepp examined trends and developments in corporate insurance, risk challenges and safety – and what it all means for our customers in a webinar on August 17.

Watch the recording here.

Allianz Group companies

The Allianz Group offers a wide range of products, services, and solutions in insurance and asset management and operates as an international insurer on almost every continent.

AGCS offices

With our worldwide network, Allianz Global Corporate & Specialty (AGCS) is one of the very few global insurers with an exclusive focus on the needs of global corporate and specialty clients.